FIFO vs LIFO: Which Inventory Method Is Right for Your Warehouse?

FIFO vs LIFO explained simply — definitions, formulas, examples, tax impact, and how your warehouse racking layout can make either method easier to run.

Every business that holds stock has to answer one deceptively simple question: when you sell a unit, which one did you actually sell — the oldest one on the shelf, or the newest one? That question sits at the heart of FIFO vs LIFO, the two most widely used inventory valuation methods in the world.

The answer isn’t just an accounting formality. It changes your cost of goods sold, your reported profit, your tax bill, and — often overlooked — how your warehouse needs to be physically laid out and racked. This guide breaks down what FIFO and LIFO mean, how they compare, and what each one actually requires from your storage system on the ground.

What Is FIFO?

What Is LIFO?

FIFO vs LIFO: The Core Difference

Assumption

Yes

Yes

This is the essence of FIFO vs LIFO accounting: same physical inventory, two different assumptions about which units left the building first — and two very different financial pictures as a result.

FIFO vs LIFO Formula

Both methods start from the same base formula:

Beginning Inventory + Purchases − Cost of Goods Sold (COGS) = Ending Inventory

Where they diverge is which purchase costs get assigned to COGS versus ending inventory.

- FIFO formula logic: COGS = cost of the oldest units sold; Ending Inventory = cost of the newest units remaining

- LIFO formula logic: COGS = cost of the newest units sold; Ending Inventory = cost of the oldest units remaining

FIFO vs LIFO Example

Say a business buys 100 units in January at $10 each, then another 100 units in February at $12 each. In March, it sells 100 units.

Same units, same sale — but FIFO reports a lower COGS and higher profit here, while LIFO reports a higher COGS and lower profit. That gap is exactly why the choice matters so much for tax planning.

FIFO vs LIFO: Advantages and Disadvantages

FIFO

Advantages:

- Matches the natural physical flow of most goods

- Simpler to track and audit

- Accepted under both GAAP and IFRS, making it the standard choice for businesses operating internationally

- Ending inventory value stays close to current market prices

Disadvantages:

- During inflation, FIFO can produce higher reported profits — which also means a higher tax bill

LIFO

Advantages:

- During inflationary periods, LIFO increases COGS and lowers reported profit, which can reduce taxable income

- Useful for businesses holding large, non-perishable, or commodity-based inventories

Disadvantages:

- Not permitted under IFRS, so it’s unusable for most businesses outside the US

- Older inventory values can become badly outdated on the balance sheet

- More complex to track and reconcile over time

Best Heavy Duty Pallet Racking Systems for Big Warehouses

✓

In an inflationary environment — where the cost of goods keeps rising — LIFO typically results in lower taxable income, because it matches your most recent, higher costs against revenue. FIFO, on the other hand, tends to report higher profit in the same environment, since it’s still costing out your older, cheaper inventory.

✓

Inventory Valuation Methods: GAAP vs IFRS

■

■

Other Inventory Valuation Methods Worth Knowing

FIFO and LIFO aren’t the only options on the table:

Weighted Average Cost Method:

Specific Identification Method:

Which Is Better: FIFO or LIFO?

How Your Warehouse Layout Supports FIFO or LIFO

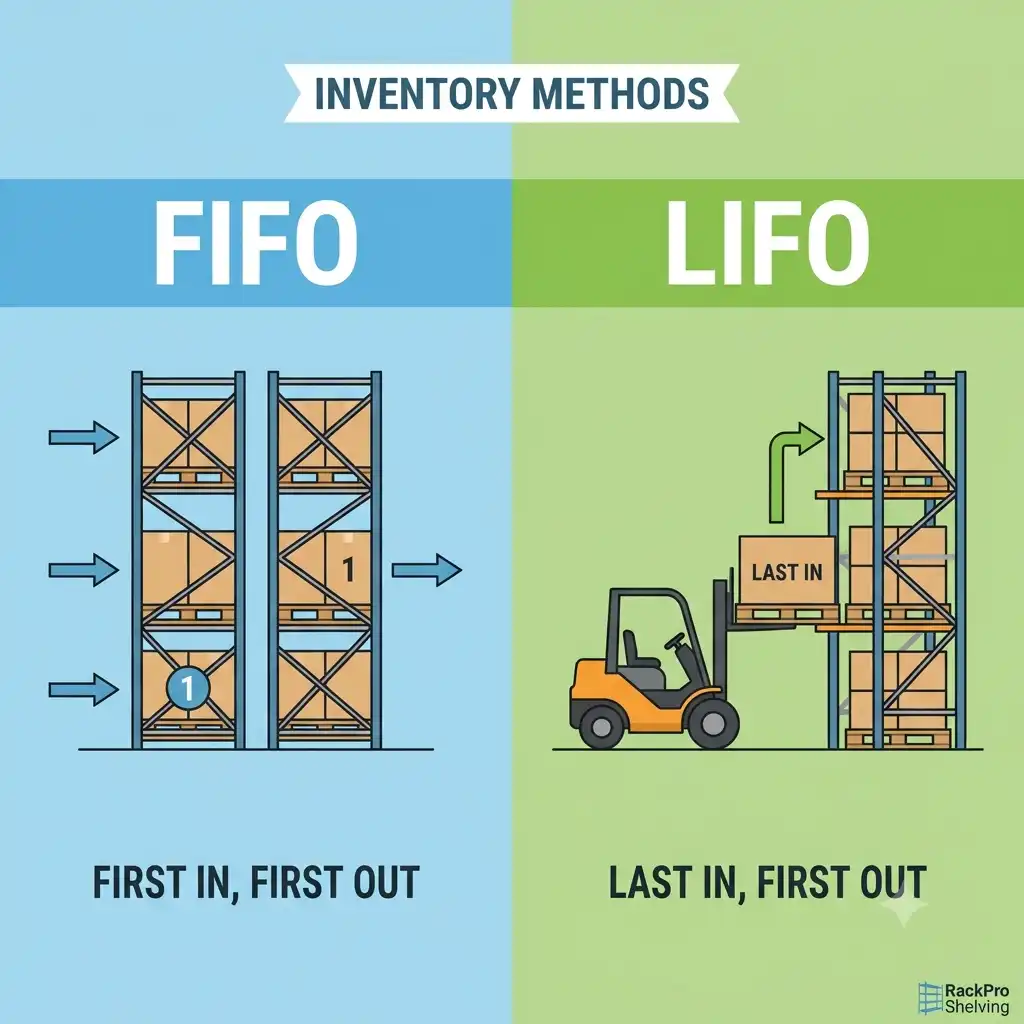

Requires racking that lets the oldest stock be picked first without digging through newer inventory. Pallet flow racking is purpose-built for this — pallets are loaded from the back and gravity-fed to the front, so the first pallet in is automatically the first one available to pick. This is the closest thing to a true FIFO racking system.

Getting this wrong creates a real operational headache: a business running FIFO accounting on paper but using drive-in racking on the floor will end up with old stock trapped behind new stock — leading to spoilage, obsolescence, and inventory records that no longer match physical reality.

If your business depends on accurate warehouse inventory rotation, the racking system isn’t a minor detail — it’s what makes your chosen valuation method actually achievable day to day. This is where working with a racking provider who understands both storage density and stock flow makes the difference between FIFO on a spreadsheet and FIFO on the warehouse floor.

Frequently Asked Questions (FAQ)

Conclusion

FIFO and LIFO both answer the same question — which inventory left first — but they lead to very different outcomes for your cost of goods sold, profit reporting, and tax position. FIFO is the global standard, required under IFRS and the more intuitive match for how goods physically move. LIFO remains a US-specific tool, useful mainly for tax deferral in inflationary conditions with non-perishable stock.